In Part I, we made the following observations:

- Spain might not be the destination to make us richer.

- If we ever plan to get a part or full-time job, we should expect a tough competitive market although our English "fluency" will come in handy.

- Given our income is based on investments, our expenses and tax burden play a more prominent role.

Cost of Living

Disclaimer: as each family has a unique set of constraints and quality of life definition, the budget and lifestyle vary. You should consider the following figures as loose guidelines and live open-ended research.

We know some families in the Dallas area - two adults and two kids - whose monthly expenses are USD 5000. This budget includes mortgage, two cars and even some travel costs. We could add USD 1200 per kid for daycare. Let's take the USD 5000-6000 budget and see how it compares to Valencia based on different information sources.

Based on Numbeo's cost of living index:

- Barcelona is 11% less expensive than Dallas

- Valencia is 22% less expensive than Dallas

- Malaga is 30% less expensive than Dallas

On Youtube, many expats living in Valencia reported their finances during 2019 and 2020. The range across all testimonies was EUR 1500-2500 or USD 1833-3056 per month, making Valencia potentially 38-70% less costly. The testimonials do not contemplate traveling, which does not represent our ideal scenario.

We have a few friends living in different parts of Spain (Madrid and Valencia). From our conversations, a family - two adults and two kids - has monthly expenses in the EUR 2000-3000 or USD 2549-3689 range. The higher side of the spectrum includes one car, full-day childcare, and a modest travel budget. Based on this, we could say Madrid or Valencia is 26-57% more affordable than Dallas.

A few highlights where the main differences might rely (Dallas vs Valencia in USD):

- rent 1800 vs 800 - ↓55%,

- utilities 300 vs 200 - ↓33%,

- groceries 600 vs 400 - ↓33%,

- private health insurance 1700 vs 200 - ↓88%,

- full-day childcare 1200 vs 450 - ↓62%,

- car insurance 141 vs 33 - ↓76%

We are not going to include the state free and subsidied full-day childcare options.

Healthcare

The national healthcare system covers 99.7% of the Spanish population. The remaining 0.3% only has access to private medical care. In addition, voluntary private health insurance has been contracted by 13.5% of the population. With USD 200 per month, we would get access to public and private insurance, no copay needed.

Education

Quality public education, realistically priced daycare and universities should be available.

In Texas, a full-time daycare costs around USD 1200 per kid. It is our understanding it costs much more in other parts of the country.

There is entirely free public daycare in Spain, and the paid options - without any state discounts - cost around EUR 450 per month.

Our knowledge of elementary and high school education in both cities is minimal. We will mention that both public options are well regarded.

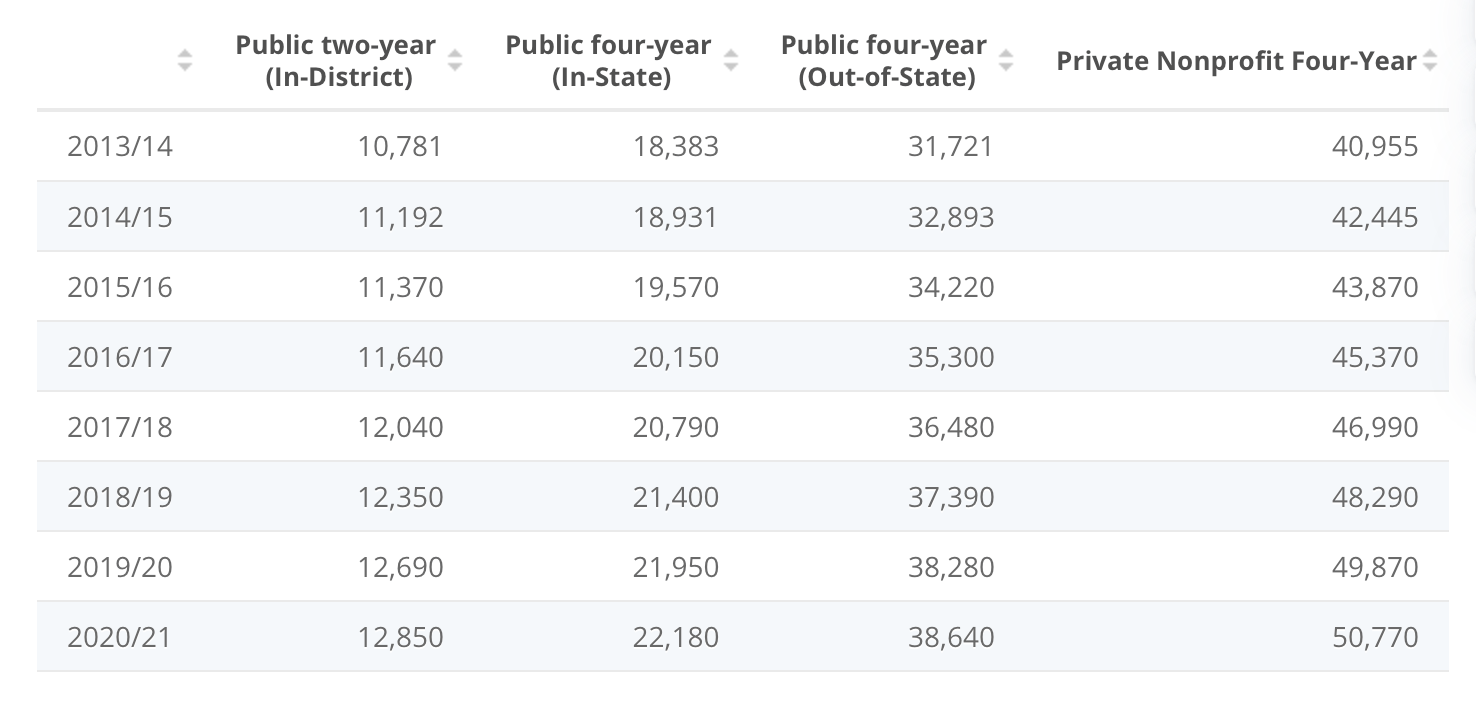

If we delve into the future, the university cost is a usual savings label in many American families via a 529 plan. Based on the US Department of Education, for the 2020–2021 academic year, annual current dollar prices at a 4-year institution for tuition, fees, room, and board were estimated to be USD 22,180 at public in-state institutions, USD 38640 at out-of-state public institutions and USD 50,770 at private nonprofit institutions.

Based on information gathered across the internet and conversations with our friends living in Spain, tuition is estimated to be USD 150-3500 per year at a public university and USD 2000-20000 per year at a private institution. Room and board costs are around USD 3000-7000 per year.

In Summary:

- At public schools, Spain is 55-82% less expensive than the US.

- At private schools, Spain is 46-82% less costly than the US.

Our observations

We feel uneasy about basing our budget forecast on testimonies. The rent, daycare, university, and healthcare costs - which we were able to verify - provide a positive indication that essential expenses are lower in Valencia. While costs may be lower, taxes might still offset the savings.

Taxes

For our taxes calculations, let's consider monthly expenses for EUR 2000-3000 euros (USD 2549-3689), which makes an annual budget for EUR 24k-36k or USD 30-44k.

Disclaimer

I'm not a tax professional neither in the US or Spain. The following debrief is based on my research online and books. This blog helps me document my research for my purposes and share it with you, hoping it will save you some time or get you on the right track. I'm using 2021 tax brackets definitions and current (Jan 2021) exchange rates for the calculations.

A few critical points about taxes in both countries:

- US and Spain both tax residents on worldwide income

- There is a tax treaty that prevents double taxation and overlapping social security contributions

Residency

If you live in Spain for 183 days in a calendar year, you are considered a resident for tax purposes. Non-residents receive a more favorable tax treatment from the Spain government. Given we would have kids attending school, we will analyze the tax obligations as residents.

Wealth Tax

Spain brings to the table a constant tax burden across both stages.

For Spain residents, the Wealth-tax is based on the value of worldwide assets on December 31st. Although Spain eliminated the wealth tax in 2009, it has since been reintroduced.

For a person filing taxes as an individual, if your wealth is more than EUR 700,000, you will be liable for a wealth tax of 0.2–2.5% on net assets. Some regions have a lower allowance. Until 2020, Valencia defined the tax-free allowance as EUR 600,000. In 2021, the Valencia region has updated the value to EUR 500,000.

This allowance is multiplied by two for a couple filing jointly, getting EUR 1M tax-free allowance.

As well as the allowance, homeowners are allowed EUR 300,000 against the value of their primary residence in Spain.

Finally, the general understanding - you should confirm with a professional - is that the wealth tax excludes retirement accounts - such as 401k and IRA - in this calculation.

As an example, for a portfolio of USD 1.5M (EUR 1.2M) minus the allowance of EUR 1M, we would need to pay taxes on the EUR 200k. The annual tax would be around EUR 600 or USD 700.

So, our annual budget goes from USD 30-44k to USD 31-45k.

Income strategy

During our retirement, we would start withdrawing money from our savings and taxable accounts. We will call this Phase I. Only when those are empty, we would move to our tax-advantaged retirement accounts. We will call this Phase II. These two sources of income are subject to different tax treatments.

Phase I

In Texas, long-term capital gains taxes for married filing jointly are 0% of up to USD 80k and 15% up to USD 500k. In Spain, capital gains are taxed at 19% up to EUR 6k and 21% up to EUR 50k.

For our USD 31-45k budget, we would not owe money in the US, but we would have to withdraw some extra to cover Spain's capital gains tax. Our updated annual budget becomes USD 40-58k.

Phase II

Once we had depleted our taxable investments accounts, we would start withdrawing from our tax-advantaged accounts. Another possible scenario is to reach a certain age without having emptied our taxable accounts. If this happens, we will have no option but to withdraw the required minimum distribution (RMD) from our retirement accounts.

While we don't have to pay capital gains on this money, traditional 401k distributions are taxed at ordinary income.

To simplify the math, we will assume our retirement account withdrawal is now our single source of income. We are back with the USD 31-45k (EUR 26-37) annual budget to cover expenses and the wealth tax.

For those married filing jointly in Texas, the first USD 20k is taxed at 10%, and from USD 20k to 81k at 12%. If we subtract the standard deduction of USD 24k, we will pay USD 0.7-2k in income tax.

Europe in general has steep taxes compared to United States. In Spain, income tax rates are as follows:

- Up to EUR 12,450: 19%

- EUR 12,450–20,200: 24%

- EUR 20,200–35,200: 30%

- EUR 35,200–60,000: 37%

- EUR 60,000–300,000: 45%

- Above EUR 300,000: 47%

Regarding deductions, a married couple filing jointly with two children under 25 years old can offset EUR 9k.

To get the net USD 31-45k (EUR 26-37k), we would need to annually withdraw an extra USD 6-13k (EUR 5-11k) to cover IRPF (income) tax and Social security contributions. There is an option to pay social security in the US instead, but we will leave it for another article.

In our scenario, the US double taxation benefit would kick in since we pay higher taxes in Spain. Our total budget - including the income tax - becomes USD 38-58k (EUR 31-48k).

A note on ROTH accounts

Based on this article:

- these need to be included on the "modelo 720" declarations of foreign assets

- these do not need to be included in the "modelo 714" wealth tax declaration.

- dividends and interest earned within the Roth IRA and Roth 401k do not need to be reported on modelo 100 income tax declaration; however,

- if you are taking distributions from these while residents in Spain, this would be considered taxable here.

Observations

The expenses will probably increase and decrease across the next fifty-five years given multiple factors (university, downsizing, etc.). For the sake of throwing a simple high-level comparison (no inflation or stocks returns simluations), a US expat retiree - now Spain tax resident -will incur the following expenses across the next fifty-five years:

- Assuming 25 years using taxable accounts withdrawing 40-58k per year, the total costs sum up to USD 1-1.45M.

- And 30 years tapping on retirement accounts at 38-58k per year, which comes to USD 1.1-1.7M.

- The total for the entire period is USD 2.2-3.15M

How would this compare if we retire in Texas?

Let's take a USD 60k annual budget (USD 5k per month). There is no wealth tax in the US. While withdrawing from taxable accounts, we would pay 60k to cover expenses, 0 USD in capital gains. Once we start withdrawing from the retirement accounts, we would need 60k to cover the costs and 1-3k USD in regular income tax.

- Assuming 25 years using taxable accounts withdrawing 60k per year, the total costs sum up to 1.5M USD.

- And 30 years tapping on retirement accounts at 61-63k per year, which comes to 1.8-1.9M USD.

- The total for the entire period is USD 3.3-3.4M

As a reminder, here is our requirement:

A destination where our living cost is the same or below the one we would have in our current location.

The living costs in Spain offset the higher taxes if you are retired. Depending on how modest our lifestyle becomes, Valencia could cost 8-40% less.

A different evaluation is needed if we start generating new significant income above our needs.

Weather, location, activities

The city should have family activities, kids' sports, public parks, and cuisine from different cultures/countries.

Given its vast history and immigrants communities, the three Spaniard cities offer an international cuisine. One thing to say about Dallas is that we also get a highly diverse cuisine given its immigrants' population.

When it comes to family activities, kid's sports, and public parks, all mentioned cities are amazing. Among expats, I kept hearing Valencia is pretty family-focused.

Soccer - football - is a family activity and the primary sport in Spain. As a soccer fan who grew up in a country that sweats the sport, I can't avoid feeling it resembles home much closer.

Ideally, the location should be by the sea and close to the mountains.

Barcelona, Valencia, and Malaga are by the sea and one to two hours from plenty of beautiful mountains.

The location should allow us to travel to many different points of interest within a three hours range.

Crossing Spain from its east sea border to its west border takes about 7 hours by car. Romans, Germanic tribes, Arabs, and Christians once ruled this country. You would have to drive blind-folded to avoid fantastic points of interest.

The weather across the year should be mild. We would accept a hot summer if we can avoid cold winters and sunsets before 6 pm.

A highly welcomed side effect comes up when we combine geography, climate, and touristic characteristics. Our friends and relatives would visit us more often. We rarely receive relative visits in Dallas, and we don't know anybody from our origin country planning their vacations in Texas or somewhere around.

We want to move back to a city or close enough to enjoy activities without using a car.

In the Dallas area, many families with kids opt to live in the suburbs. We live about one hour drive away from the city (40 miles - 65 km). We could move to the city with the increased living cost and basic public transportation. We once did a staycation - spend a weekend in a hotel in the same city/area you live in - and found that the city was rather desolated during non-business hours or days.

Barcelona would be the absolute opposite, always crowded with tourists every single day of the year. Valencia has the metropolitan feeling without being infested neither by people or cars. Malaga is more lay back, smaller city feeling and experience.

We believe we can dispense with having a car in Valencia and Malaga, potentially renting one for road trips only. If we were to travel often, then we might need the vehicle.

Conclusion

As we collect more information, we understand the tradeoffs, review our decision and walk more confidently towards Spain.

Our decision should be irrelevant to anybody but us. We sincerely hope to share as we learn and learn from others' experiences.