Today, six years later, our goals have changed. We are now considering moving abroad in a few years, which would entail selling our house sooner or later. Or should we rent it? "Sell vs. Rent" is a topic for another article. We are going to assume selling is the path ahead.

During May, given the low-interest record rates, we refinanced our home, reducing the long-term cost substantially. Kudos to us! We also replaced the AC/Furnace. We could have postponed it for a year or two, maybe longer.

During August, I've read "Quit like a millionaire" by Kristy Shen and Bryce Leung. A well-written book. In one of the chapters, the author guides us over a math exercise on why renting could be a better option than taking a mortgage loan. It implies adding up all ownership expenses on top of the principal and interest you pay for the walls and roof you've acquired. It sounds pretty similar to my 2014 spreadsheet. Here is the catch. Statistically, in the US, people move out within nine years, and so the author includes commission and fees for selling the house in the calculation.

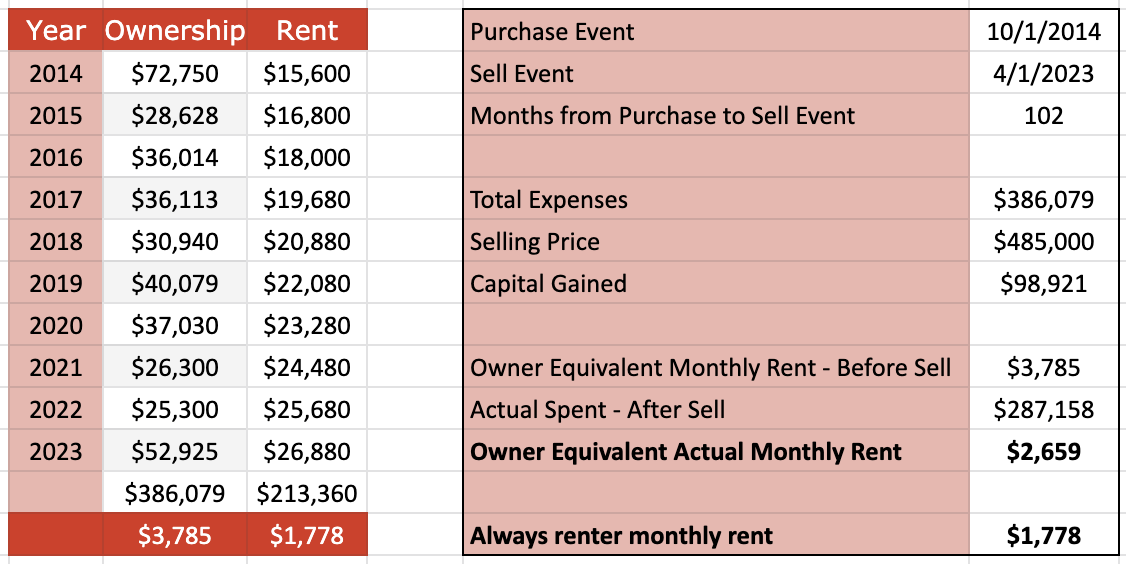

Naturally, I now know what those expenses across these six years were, so I thought it would be an interesting exercise to understand the actual cost of living in our home. Using Zillow's property estimated value, calculating 6% commission, standard fees, and projecting costs for the next two years and three months:

We've paid $3785 USD per month to live in our house since 2014. This amount is $500 USD higher than the rent value I can find today for similar homes in our neighborhood. I would imagine the cost would have been much lower in 2014. Ouch!

It gets worst when I look at the rent column. Including rent, tenant's insurance, covered parking, and washer/dryer rental, the average monthly cost comes to $1778 USD. During these six years, I'm taking rent increases yearly and make a few jumps as our kids were born, and we needed the extra room.

Our house, its beautiful large backyard, and mature trees worth more than $1778 USD in all fairness. We have enjoyed it. We look outside the window and feel fortunate. Nevertheless, I don't think our life quality or happiness would have been drastically different if we had lived in an apartment these last six years. We still have rooms without furniture or that we hardly use. Even if we had rented a similar house it like we could have saved significant money.

If we take into account the house has increased its value, we would get almost 100k out of the sale. If we substract this amount from the total paid so far and recalculate the actual monthly average cost; we get $2659 USD. We may conclude we are paying $2659 USD for a $3200 USD house. Yay! We may also say we are paying around $700 USD more than if we were renting an apartment.

What is your case? Punch in your numbers and get the answers.

| Year | Ownership | Rent | Edit |

|---|---|---|---|

| 2014 | 70000 | 1400 | |

| 2015 | 28000 | 1500 | |

| Enter Year | Enter Ownership | Enter Rent |

| Enter data | |

|---|---|

| Purchase Event | |

| Sell Event or (leave as today) | |

| Selling price | 0 |

| Results | |

|---|---|

| Capital gained | 0 |

| Actual Spent - After Sell | 98000 |

| Months | 76 |

| Total Ownership Expenses | 98000 |

| Owner Equivalent Monthly Rent - Before Sell | 1289 |

| Owner Equivalent Actual Monthly Rent - After Sell | 1289 |

| Always renter monthly rent | 38 |

What a big mistake! Yes? No?

In my case not really! I did the math back in 2014, given all data and knowledge at my disposal. We are at peace.

My actions and not my past define me; there is time to math this shit up once again and course correct.

Assuming we sell our home in two years, the question becomes, "should we sell now and move to an apartment or sell at the end of the two years?".

Part II - Sell vs Rent

Cons of selling "now":

- Packing and unpacking is hell.

- Kids need to adapt.

- We may need to find a new daycare more convenient to our new location.

Pros of selling "now":

- We can move closer to the city and experience more attractions.

- We can save money by accelerating our path to FI.

- It forces us to get rid of a lot of junk.

- We can taste what life abroad would look like as it would entail an apartment and not a house.

When it comes to saving costs, you might think we would save a whopping $700 USD per month if we move out now. In reality, many of the significant expenses such as the down-payment or big repairs already happened. For the next two years, the onwership cost would average around $2150 USD per month.

If we were to rent today a three bed apartment, the cost would be $2000 USD per month, including parking, insuranced and other expenses. Let's assume next year the total package increases by 5%. That's a monthly average of $2050 USD.

Mmm...so the cost on both equations is pretty close. Are we staying then? Not so fast. There is one more dimension to the story.

After we had paid the remaining loan, commissions, fees, and taxes, we would still have a healthy 200k to pour into our taxable investment account. According to Goldman Sachs, 10-year stock market returns have averaged 9.2% over the past 140 years. In the last 10 years (2010-2020), the S&P 500 had an annual average return of 13.6%. If we assume a conservative market growth of 5% per year, we could get ~10k before taxes in the first year , hold them long-term and sell in a lower tax bracket future. If we estimate a 9.2% return, we can expect 18k before taxes. Alternatively, We could invest in Bonds - such as FXNAX - to reduce risk and volatility with a 10-year average return of 3.60% providing 7k before taxes.

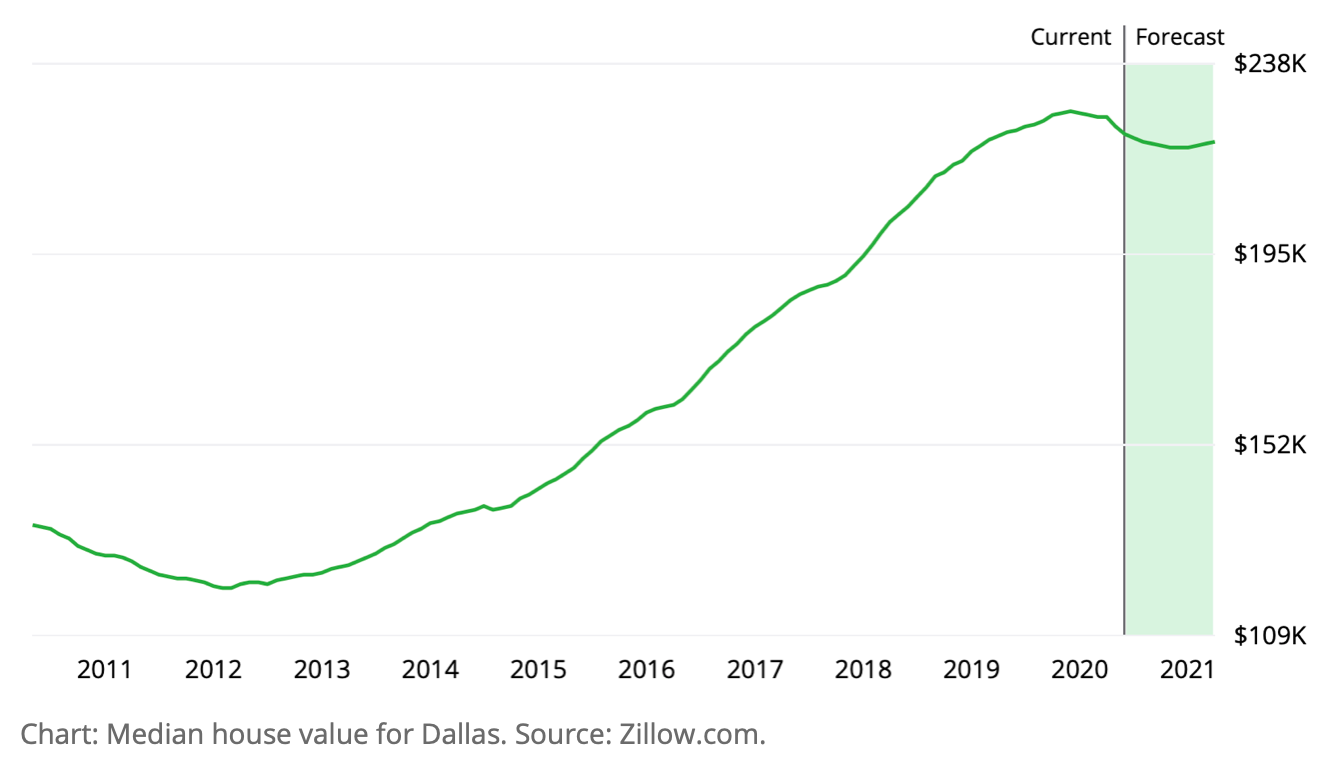

If we keep the house, its value could increase. The DFW housing market has steadily grown during the last seven years (2.4% every year). Zillow's housing forecast predicts that home prices will decline by -1.9% over the next 12 months. So we could see a variation of -9k to 11k.

"Past performance is no guarantee of future results".

Given we have uncertainties and forecasts, the scenario does not provide a straight forward conclusion, and it relies more on the consumer's ability, willingness, and need to take the risk.

- If we want to play it "safe", we should sell and invest on BONDS.

- If we belive our income's sources are steady, we should sell and invest in stocks.

Is there any scenario where we should stay? I think there is. Not everything is quantifiable. Our family loves this home, our kids are growing and enjoying the open space every day liltle bit more. I could and should do more barbecues! Last but not least, there is a freaking pandemic going and we dont need the stress of packing, selling things, moving, unpacking, adapting.

In our case, I think we will postpone the question until the global situation clears up. In the meantime, we will arrange some apartment's tours to see what life would look like.